TEXTILES.ORG

TEXTILES.ORG

As consumer confidence slowly increases, buoyed by improvements in the U.S. economy and employment figures, respondents in 10 of the 11 markets surveyed by IFAI predict single-digit increases in sales in 2016. Innovation in products and processes will help manufacturers anticipate customer needs and stay competitive in a global economy.

Part I of IFAI’s 2016 State of the Industry article discussed key markets, issues and trends in the U.S. and global specialty fabrics marketplace. It also presented an overview of five key end-product market segments in the specialty fabrics industry—awnings and canopies, marine fabrication, fabric structures, fabric graphics, and tent rental and manufacturing. In Part II, we focus on six additional markets, primarily in the United States: military applications, advanced textile products, narrow fabrics, geosynthetics, tarpaulins and truck covers, and industrial fabric equipment.

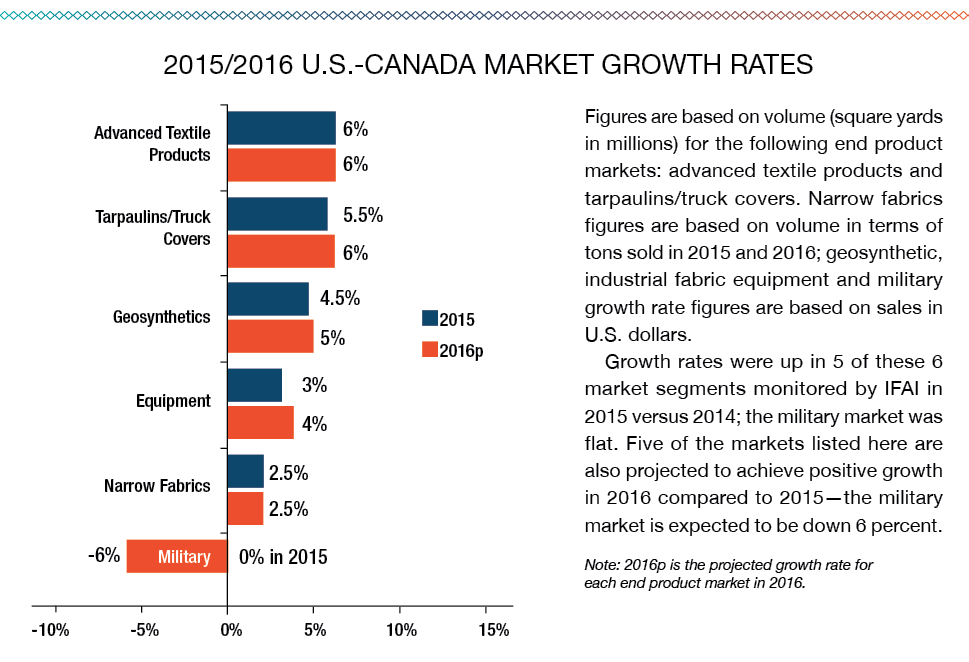

All but one of these six end product market segments IFAI monitors achieved single-digit sales growth in 2015—the military market was flat. Investing in state-of-the-art equipment, lean/quality improvement manufacturing practices, training staff and vastly improved marketing efforts targeted toward the customer have helped organizations increase sales and profit margins.

Key Markets

Military

The U.S. military market covers safety and protective products (including the use of smart technology) for troops, firefighters and law enforcement. A driving force behind product development for the firefighter, law enforcement and industrial markets, the military’s influence on the safety and protective market will continue through 2016. Due in large part to the withdrawal of most U.S. troops deployed in Iraq and Afghanistan before 2015, spending on U.S. military textiles and clothing is expected to decrease by 6 percent in 2016, but is still expected to reach about $1.5 billion.

Spending on U.S. military textiles and clothing is expected to decrease by 6 percent in 2016; but the level of spending on military textiles and clothing is still expected to come in at a substantial amount—estimated to be about $1.5 billion.

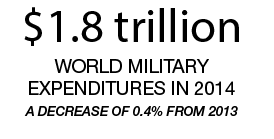

World military expenditures totaled $1.8 trillion in 2014, a decrease of 0.4 percent from 2013. The U.S. is the leading military spender in the world, representing 34 percent of the global market—spending $610 billion in 2014, $601 billion in 2015 and a projected $607 billion in 2016, up 1 percent from 2015. The U.S. outspends the seven next-highest spending nations on defense, which include China, Russia, Saudi Arabia, France, the United Kingdom, India and Germany.

While total world military spending is mostly unchanged, some regions, such as the Middle East and much of Africa, are continuing to see rapid build-ups that are placing an increasing burden on their economies. The conflict in the Ukraine is prompting many European countries near Russia, in Central Europe, the Baltics

and the Nordic countries, to increase military spending.

The Ukraine increased spending by more than 20 percent in 2014, nearly doubled spending on its armed forces in 2015, and is likely to significantly increase spending in 2016. The continuing crisis there has fundamentally altered security readiness in Europe, but so far the impact on military spending is mostly apparent in countries bordering Russia. Russia’s defense budget for 2016 is set to increase 0.8 percent from 2015. The government continues to carry out a $700 billion military modernization project established in 2010; the goal is to replace 70 percent of Soviet-era military hardware by 2020.

Military expenditures in Asia and Oceania rose by 5 percent in 2014, reaching $439 billion. The increase is mostly accounted for by a 9.7 percent increase by China, which spent an estimated $216 billion. In 2015, China reported a military budget of $141 billion; off-budget military spending was $78 billion—creating a total military budget of $219 billion.

Military expenditures in Asia and Oceania rose by 5 percent in 2014, reaching $439 billion. The increase is mostly accounted for by a 9.7 percent increase by China, which spent an estimated $216 billion. In 2015, China reported a military budget of $141 billion; off-budget military spending was $78 billion—creating a total military budget of $219 billion.

Among other major military spenders, Australia increased spending by 6.7 percent, with smaller increases by South Korea and India of 2.3 and 1.8 percent, respectively. Japan’s spending remained steady. Vietnam, with tensions with China over territorial disputes in the South China Sea, increased spending by 9.6 percent.

It’s unclear what impact the sharp fall in the price of oil in 2015 may have had on the large increases in military spending that have taken place in many oil-producing countries in the Middle East, parts of Africa and Asia and Russia, among others. While some producers, such as Saudi Arabia, have built up large financial reserves that will enable them to withstand lower prices for some time, others may be more affected—for example, Russia reduced its military spending plans for 2015 accordingly.

Advanced Textile Products

Growth in the U.S. advanced textile products market was up 6 percent in 2015, and is expected to increase another 6 percent in 2016. Growth was buttressed by a noticeably improved job market in 2015—with unemployment reaching 5.3 percent (versus 6.2 percent in 2014). The U.S. manufacturing sector has remained stable over the past three years. In fact, according to the 2015 Institute for Supply Management (ISM) Manufacturing Report on Business poll of U.S. supply executives, in terms of America’s manufacturing sector, the overall economy has grown for 78 consecutive months.

Growth in the U.S. advanced textile products market was up 6 percent in 2015, and is expected to increase another 6 percent in 2016. Growth was buttressed by a noticeably improved job market in 2015—with unemployment reaching 5.3 percent (versus 6.2 percent in 2014). The U.S. manufacturing sector has remained stable over the past three years. In fact, according to the 2015 Institute for Supply Management (ISM) Manufacturing Report on Business poll of U.S. supply executives, in terms of America’s manufacturing sector, the overall economy has grown for 78 consecutive months.

Outlook for the advanced textile products market. Going forward, suppliers and end product manufacturers in the U.S. advanced textile products market will see improved sales in 2016 due to a steadily improving economy and the higher employment figures over the past few years. Confidence in a sustained expansion of the U.S. economy has grown strong enough that in mid-December 2015, the Federal Reserve raised its benchmark federal funds interest rate from zero to a range of ¼ to ½ percent, its first rate increase since June 2006. (The federal funds rate is the amount that banks charge to lend to each other overnight; the rate increase was executed due to strong improvement in the U.S. labor market, and to hold inflation at or below its target rate of 2 percent.)

Markets like military clothing, construction and industrial applications—especially the automobile/industrial market—will continue to drive growth in the advanced textile products market in 2016. In a survey of IFAI advanced textile products members in November 2015, one trend both suppliers and end product manufacturers cited in 2015 (and expect to continue to see in 2016) is strong sales growth in the high-temperature, flame-resistant products market—especially in the military and firefighter arenas.

Narrow Fabrics

IFAI focuses on five key market segments in the narrow fabrics market: webbings for automotive seat belts; military textiles and clothing; safety products such as harnesses; transportation products such as tie-downs and slings; and medical products such as wound care (gauze and bandages).

The narrow fabrics industry in the U.S. continues to consolidate. Competition among market participants is fierce. To maintain and improve one’s place in the narrow fabrics marketplace, companies must find ways to grow and compete through the development of new technologies and products, as well as identifying and competing in new markets on a global scale.

The overall U.S./Canadian narrow fabrics market grew an estimated 2.5 percent in 2015; it is expected to grow 2.5 percent again in 2016. The main growth area over the last few years has been webbings for seat belts in the automotive market. Technological advancements such as sensors embedded in seat belt webbings are showing great promise for new products such as smart, inflatable seat belts and seat belts that warn drowsy drivers. Sales of new light vehicles in the U.S. grew 6 percent in 2015—reaching 17.4 million vehicles, which translates into 261 million meters of seat belt fabric sold.

Growth in spending on military textiles and clothing in the U.S. was flat in 2015 compared to 2014. The Department of Defense (DoD) and the Defense Logistics Agency (DLA) are concerned that sequestration caps on the military budget in 2016 will inhibit the level of spending; the DLA expects spending on textiles and clothing will decrease to $1.5 billion in 2016.

The market for safety products (safety or fall-control harnesses in particular) grew 4 percent in 2015 as growth in the U.S. construction market picked up significantly in 2015. That market was buttressed by President Obama’s signing of a 5 year, $305 billion highway bill on December 4, 2015, which should help the safety products market grow 5 percent in 2016.

Tie-downs and sling sales in the transportation market are growing, despite the continuing effects of inexpensive imports from China and Korea. As in the safety harness market, the new highway bill should fuel growth in the tie-down and sling market, which could see 4 percent growth per year over the next 5 years.

The medical products market grew 5 percent in 2015, and is expected to grow another 5–6 percent in 2016. Seventy-five million baby boomers in the U.S. serve as a key impetus for growth; approximately 83 million millennials (people born in the 1980s and 1990s) in the U.S. are also adding to growth in the medical narrow fabrics market. Younger and older people are spending more money on new, innovative smart narrow fabrics products. Examples can be found in the fast growing sports and fitness monitoring market—the fastest growing smart fabric market in the U.S. in 2015—growing at 40 percent per year. People that are middle-aged and older are spending more on wearable medical products that monitor a patient’s heart rate, pulse and other vital signs.

Other developments in narrow fabrics include technological advancements in composites, where the weight-to-strength ratio of these materials has and will continue to increase their usage in the automotive and aerospace markets.

Geosynthetics

The U.S./Canadian geosynthetic market includes geotextiles, geomembranes, geogrids, geosynthetic clay liners, drainage materials, geocells and erosion control materials. In 2015, the size of the U.S./Canadian geosynthetics market was $2.3 billion, an increase of 4.5 percent from 2014. The market is expected to swell to $2.4 billion in 2016, up 5 percent compared to 2015. In a survey of Geosynthetic Materials Association (GMA) members and nonmembers in November 2015, respondents reported they expect sales to be moderately better in 2016 than in 2015.

The U.S./Canadian geosynthetic market includes geotextiles, geomembranes, geogrids, geosynthetic clay liners, drainage materials, geocells and erosion control materials. In 2015, the size of the U.S./Canadian geosynthetics market was $2.3 billion, an increase of 4.5 percent from 2014. The market is expected to swell to $2.4 billion in 2016, up 5 percent compared to 2015. In a survey of Geosynthetic Materials Association (GMA) members and nonmembers in November 2015, respondents reported they expect sales to be moderately better in 2016 than in 2015.

TRENDS CITED IN THE SURVEY

Due to subdued growth in economies across the globe in 2015 and 2016, U.S. geosynthetic manufacturers will likely experience stiffer competition for sales due to more inexpensive imports coming into the United States

U.S. Environmental Protection Agency (EPA) enforcement of lining coal ash sites has led to an increase in sales for the geomembrane market; in tandem with the lining of coal ash sites, the increase of lining solid waste sites in the U.S. has led to 7–10 percent growth per year in the geomembrane market

Increased closings of coal ash sites are anticipated, especially those sites not in compliance with EPA regulations.

OPPORTUNITIES CITED BY SURVEY RESPONDENTS

OPPORTUNITIES CITED BY SURVEY RESPONDENTS

- An increase in growth of the geosynthetics market through continued industry efforts to improve and promote the benefits of geosynthetic usage to state DOTs.

- Continued efforts to educate civil engineers about the benefits of geosynthetic usage compared to traditional building materials.

- The passage into law of a 5-year U.S. highway bill in December 2015 should be a boon for the geosynthetics market in terms of road and bridge construction projects across the U.S.

- More geotextile manufacturers are becoming compliant with the National Transportation Product Evaluation Program (NTPEP), helping to boost the quality and credibility of geotextile prime and private label manufacturers in the eyes of state DOTs and civil engineers across the U.S. Compliance helps geotextile manufacturers to better compete with traditional materials manufacturers for future road and bridge construction projects in the U.S.

INDUSTRY OUTLOOK

On December 4, 2015, President Obama signed a 5-year highway bill titled “Fixing America’s Surface Transportation Act” (or FAST Act). It prevents the insolvency of the Highway Trust Fund, which was due to run out of funds just hours after he signed the bill. This is the first long-term national transportation spending package since 2005, ending the pattern of short, stopgap funding fixes that we’ve seen over the past 10 years. FAST Act is important to the U.S. geosynthetics market for a variety of reasons, but the most important may be its inclusion of a geosynthetics amendment, which reads as follows:

“To the extent practicable, the Secretary of Transportation shall encourage the use of durable, resilient, and sustainable materials and practices, including the use of geosynthetic materials and other innovative technologies, in carrying out the activities of the Federal Highway Administration.”

The FAST Act places the U.S. geosynthetic market on the path to 6 percent annual growth for the next handful of years.

Tarpaulins and Truck Covers

Applications for tarpaulins range from hay tarps to tarps used in the waste industry as well as the military. One of the most commonly used tarps is the polyethylene or poly tarp. Because these tarps are waterproof, strong and durable, they’re often used on construction sites, as well as for boat covers, campgrounds, roof covers, machinery covers and similar uses.

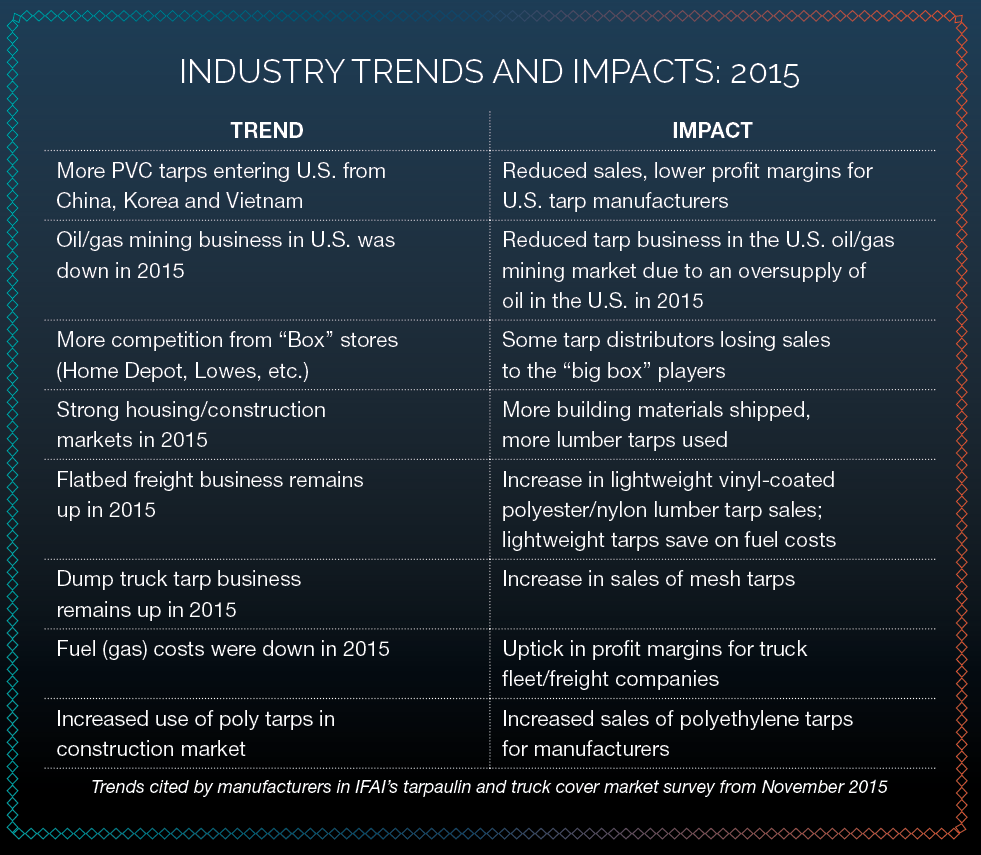

Tarpaulins and truck covers (also referred to as truck tarps) are distinctly different product segments. Truck covers are designed to fit a specific type of load and truck; they are custom made and designed to cover and protect freight on different types of trucks for transportation applications. In a survey of IFAI tarpaulin members and nonmembers in November 2015, respondents noted a number of trends and their impacts on the 2015 U.S. tarpaulin and truck cover market (see sidebar).

Outlook for 2016. In the November 2015 survey, respondents reported they expect sales to be somewhat better in 2016 versus 2015. They also cited market developments they feel will facilitate an improved tarpaulin/truck cover market in 2016. These developments include:

- The transportation construction market is growing again—expect 4 percent growth in 2016; this will continue to fuel demand for lumber and steel tarps; poly and mesh tarps will continue to be popular.

- The tarp repair business will continue to be an important source of revenue for many tarp and truck cover shops; for many, it contributes up to 25 percent of their annual revenue.

- The U.S. tarpaulin/truck cover market will remain very competitive; expect price pressures from domestic and foreign competitors to win business in 2016.

- Tarpaulin/truck cover businesses will continue to experience a shortage of skilled truck drivers.

There is a growing concern on the part of tarpaulin manufacturers and truck fleet/freight companies regarding the increased enforcement activities from OSHA and state governments pertaining to regulatory restrictions on the use of standard tarps, especially safety regulations regarding the transportation and storage of goods. The increased enforcement of truck tarp regulations by state governments has been a by-product of state governments seeking to find new ways to offset lower tax revenues.

The U.S./Canadian tarpaulin and truck cover market grew 5.5 percent in 2015 and should achieve 6 percent growth in 2016 as the U.S. economy continues to improve.

Equipment

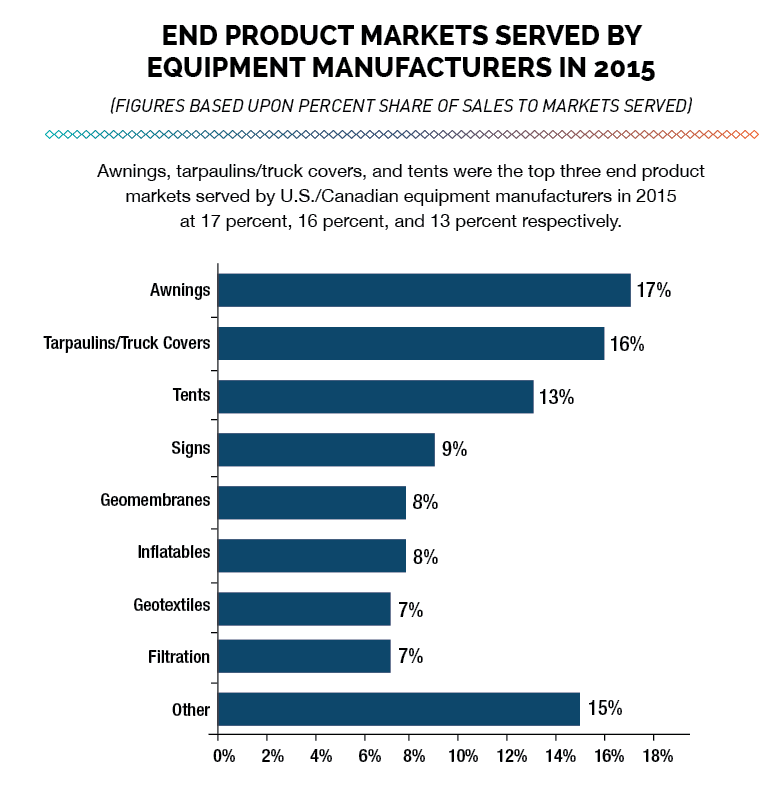

The U.S./Canadian industrial fabric equipment manufacturer market includes fabric equipment for cutting, heat sealing and welding, printing and graphics, labeling and marking, grommeting, pattern making, sewing, slitting, tables for cutting and sewing, testing and more. In terms of value, this market was $546 million in 2015, an increase of 3 percent over sales in 2014. It is expected to grow by 4 percent in 2016—reaching about $568 million. In a survey of IFAI equipment manufacturer members in November 2015, respondents ranked the top end product markets they served in terms of sales in 2015. The results are shown in the accompanying table on this page.

Survey respondents also reported they expect sales to be better in 2016 than in 2015. An increase in the automation of equipment used was a key trend cited by respondents—especially the automation of sewing equipment.

Another trend cited in the survey was the noticeable growth in the use of banners and soft signage, particularly point-of-purchase signage in retail settings, and the greater use of tension banners at trade shows. More end product manufacturers are investing in direct printing on fabric, allowing them to print on fabrics as they run on cutters and automated sewing machines. This seems to be the key for industrial fabric equipment manufacturers in the future—providing end product manufacturers with highly flexible, customized equipment aligned directly to the customers’ manufacturing requirements.

Another notable, if gradual, change in the market is that more equipment manufacturers seem to be reshoring their manufacturing facilities back to the United States and Canada after spending years operating overseas.

Industry Outlook

Industry leaders continue to invest in new product development and improving internal business processes such as supply chain logistics and automated-programmable cutting and sewing equipment, as well as six sigma lean manufacturing programs. These investments have enabled U.S. manufacturers to become more competitive with imports from companies in countries like China and India; as the costs of production and labor continue to escalate in China, the ultimate result is greater parity with U.S. manufacturers.

The most successful specialty fabrics organizations emphasize continuing innovation as a key component in the organization’s business model. These companies serve as a guide for other businesses throughout the industry on how to design and develop a successful business model (or models) now and in the future. Some participants in our industry continue to lament the loss of sales from inexpensive imports. By employing innovation as the basis for developing products and competing in general, more specialty fabrics businesses in the U.S. and Canada can reduce the negative effects of overseas competition and return to steady growth.

Jeffrey C. Rasmussen is IFAI’s market research manager; jcrasmussen@ifai.com, +1 651 225 6967.